Last Updated 10.25.23

In this age of global warming-aggravated extreme weather events, any rational individual or business will not want to invest in real estate in a high-risk climate change location that will be regularly (or permanently) disabled by repeated climate catastrophes. Climate catastrophes have many faces, like the hurricanes of Harvey, Irma, and Marie, or the wildfires of Northern California that burned over 6,000 structures, droughts in the west, or storm and sea level flooding occurring worldwide.

The illustration below shows only a few of the consequences of climate change and global warming.

It is not just extreme weather events like heatwaves, heat domes, droughts, sea level rise, wildfires, hurricanes, flooding, rain bombs, extreme winds tornadoes, (Derechos), dust storms, wildfire smoke storms, and freak cold spells and non-seasonal weather and those severe costs that will determine the best future locations to buy or sell real estate for personal use or investment or to conduct or build new businesses. Unlike many of our climate-denying politicians, smart real estate investors and businessmen now understand that they must plan their future real estate investments and business operations and investments only where the 20 worst consequences of escalating global warming will be minimized. Smart real estate investors and businessmen have also noted that our military and intelligence agencies have repeatedly warned that escalating global warming has become the greatest disrupter, threat, and risk multiplier of the 21st century.

Because global warming has become the great disruptor of the 21st century, the minimal due diligence criteria and 7 new rules for evaluating where and when to plan, buy or sell personal or corporate real estate have now become:

1.) Do not buy or own property in areas near forests because of increasing wildfire and smoke danger due to the escalating temperatures, droughts, and increasing atmospheric heat turbulences (today's ever-increasing heat creates higher future winds to fan and rapidly spread the fires).

2.) Do not buy or own property or businesses or create new businesses in areas projected for global warming-intensified extended droughts areas because of life-stifling heat, predicted massive water shortages, and as mentioned above, wildfires. These droughts and intense heat waves will increasingly slow and interfere with normal commerce.

3. Do not buy or own property in any millennial floodplains. Millennial floodplains are the newly calculated floodplain maps that most insurance agencies are rapidly creating and using to replace the no longer useful or even applicable 100-year-old floodplain maps. We are now looking at superstorms of all kinds, and other severe weather events that used to occur only several times per thousand years occur numerous times every decade because of the escalating global warming emergency. These thousand-year millennial superstorms also flood completely new areas close to rivers and lakes. This new shift to using the new millennial floodplain maps also means that insurance companies will be radically raising rates for many of their new millennial map expanded floodplain customers and canceling others altogether. The release of these new insurance company millennial floodplain maps will also radically and suddenly affect real estate property values once they become widely publicly known, as they soon will be.

4.) Do not buy or own property or businesses or create new businesses in areas projected to have regular global warming-caused or aggravated “rain bombing” where a month’s or week’s worth of rain falls in a single day or several days and seriously floods inland areas many of which have never previously flooded in this way. Rain bombs will cut normal commerce and transportation in an area from days to weeks and even months.

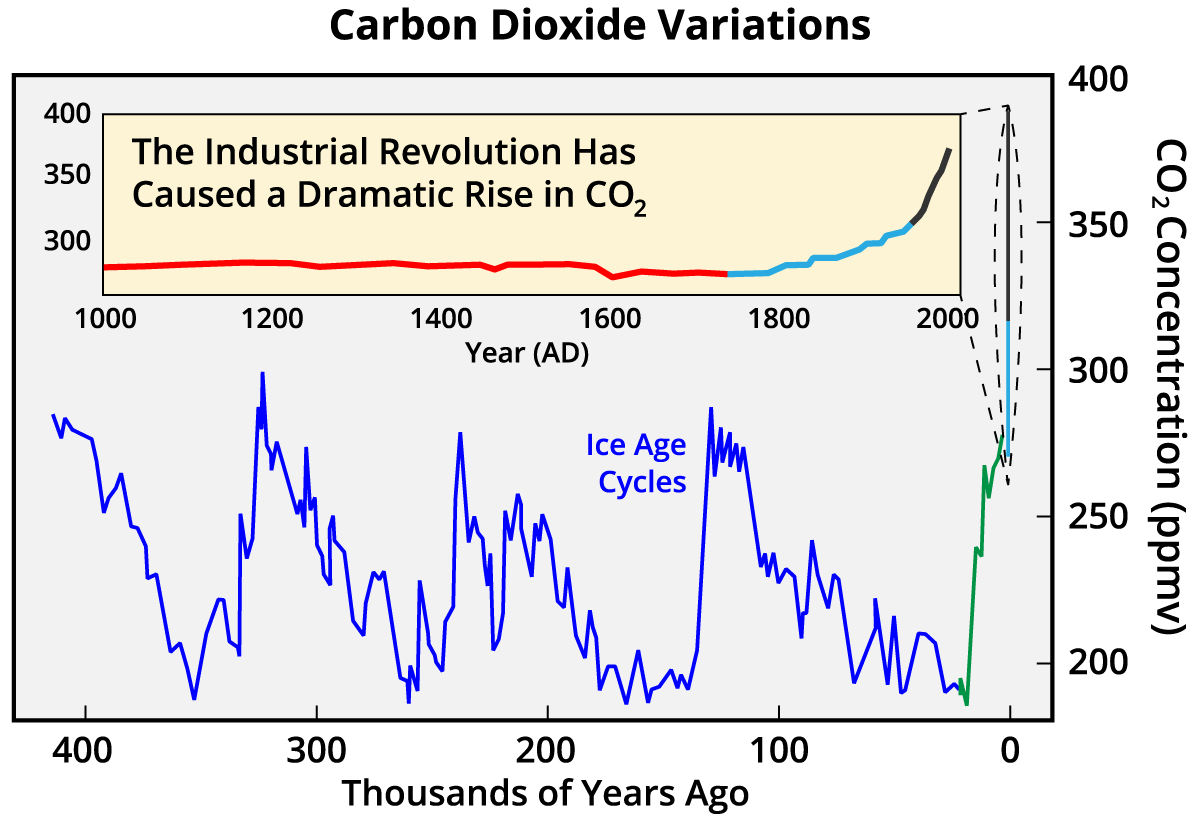

5.) Do not buy or own property less than 25 feet above sea level if you are considering coastal areas. This new real estate investment rule will take a little technical explaining. The carbon level in our atmosphere in parts per million is the single best and most accurate way to tell if we are progressing in reducing or slowing global warming. As of March 2022, we are at 421 carbon parts per million (ppm), with an average increase of 4 more carbon ppm each year. As you can see in the carbon ppm graph below, things are getting worse at an exponential rate by the trend line!

At 421 carbon ppm, the stability of the bellwether West Antarctic ice sheet has already been breached and is now irreversible.

At the carbon 425-450 ppm threshold, which we will hit in about 4-10 years, we will continue crossing more of the 11 critical global warming tipping points within the many systems and subsystems of the overall climate, but now at an even faster rate.

Moreover, once we cross the carbon 500 ppm threshold, projected around 2040 (about 23 years or less from now,) ALL ice and ALL glaciers on Earth will go into complete meltdown and the oceans will eventually rise by 70 meters (230 feet). This has happened repeatedly in Earth's geological history whenever carbon levels crossed this critical carbon 500 ppm atmospheric threshold.

When we re-calculate sea level rise, which now will include crossing one or more of the 11 critical global warming tipping points, these new calculations and allowances predict as much as a 3-meter (10 foot) global sea level rise by 2050. This is not the publically promoted three-foot sea-level rise by 2100 put out by the UN’s Intergovernmental Panel on Climate Change. Unfortunately, the IPCC has repeatedly underestimated global warming impacts by 20 to 40% and has utterly failed to properly include calculations for crossing any of the significant global warming tipping points now in play.

This means that if you are planning to purchase any piece of real estate near sea level, you want it to be safe and the property to be viable past at least 2050; for a minimum level of sea level safety, the property would need to be 10 feet above sea level, plus the height of the local king tides and storm surges normal to that area, plus an extra safety measure to ensure your real estate investment will be around for more than 50 years. (It is important to note that several times in Earth’s geologic history, sea levels have risen by 10 feet or more in as little as two decades after significant climatic tipping points were crossed.)

The following graph will help illustrate the future problems of our currently rising atmospheric carbon dioxide and carbon ppm levels in the atmosphere from a perspective of hundreds of thousands of years. As you can see in the last part of the graph, which has been broken out to illustrate our last 1,000 years better, it clearly shows we have entered a whole new range of increased atmospheric carbon security risk and threat exposure.

For hundreds of thousands of years through various Ice Age cycles, we stayed below about 275 carbon ppmv. But since the beginning of our extensive use of fossil fuels starting with the Industrial Revolution, atmospheric carbon levels and average global temperatures have soared to levels we have not seen for millions of years!

Image via Robert A. Rohdes, Wikimedia Commons. (Parts per million by volume [ppmv] includes other pollutants and trace greenhouse gases, such as methane.

If you currently own or are considering buying any real estate or businesses not above 13 feet above sea level near a coastal area, don't unless you plan to flip the property within a very short period and long before 2050. Sea level rise will impose massive, rushed infrastructure rebuilding costs for relocating or rebuilding electrical, sewage, harbors, sea walls, bridges, highways, and water in all coastal areas less than 13 feet above sea level before 2050. Residents and businesses who don't want to spend the retrofitting cash will significantly drop their sale prices to cash out and move to safer areas. Military bases, particularly naval bases that are located in areas less than 13 feet above sea level, will be particularly hard hit in that they will not be able to perform their normal protection, resupply, and repair functions due to regular and escalating flooding.

6.) Whenever possible, seek to locate significant real estate and business investments in areas near or above the 45th parallel north or near or below the 45th parallel south. In computer models, these areas are projected to be the safest if they have adequate water and decent soils.

Ever-increasing heat, security issues, and the other global warming consequences like rain bombs, drought, massive crop failures, and water shortages will continue to create a massive “climagee” (climate refugee) migration from the ever-expanding global warming crisis to unsafe zones below the 45th parallel north.

These climagee migrations are predicted to begin in earnest from about 2027 through 2040 as the general population realizes they have been mislead about how bad global warming is and how bad it will get. These migrations will involve first hundreds of millions, and then billions of individuals with few or no resources as the catastrophic reality of escalating and out-of-control global warming wreaks havoc below the 45th parallel north and above the 45th parallel south, and it becomes undeniable to the majority of the world’s population. It is highly doubtful that real estate businesses or personal investments in zones that will be inundated with hundreds of millions of desperate climagees will be able to maintain their value or continue doing anything like business as normal.

7.) Soaring flooding, fire, crop, and storm insurance prices, and the inability to get mortgage insurance because of increasing refusal of insurers to offer insurance and global warming unsafe zones. As more people recognize global warming location as the new big factor in property valuation and business investment viability, and as more insurance companies raise rates and deny coverage in more global warming unsafe zones, real estate values will, on average, begin losing or gaining about 1% to 3% of their value each year depending upon whether you're in a global warming safe or unsafe location. (In many areas of Houston, Texas, after its last big storm, real estate values have dropped as much as 7% in one year.)

Property values will soar or crash much faster in some global warming safe or unsafe zones. In spite of the difficulty of predicting exactly how much property values will rise or fall, with few exceptions, the more an area is recognized by more people and insurance companies as a global warming unsafe area, the faster real estate property values will continue to drop and vice versa.

Please click here to see our new article on all the reasons for the avalanche of new insurance company climate change-related cancellations, denials, and soaring rates for home, business, mortgage, and farm crop insurance.

8. A new bonus rule: The world's largest real estate price crash is coming. If you have not done so already, please take the time to read about one very hazardous glacier collapse that will near-instantly radically change the price of costal real estate around the world. It is also genuinely critical to your immediate and future well-being.

Click here to read about the 2-3 foot quick and severe global sea level rise consequences of the Thwaites "doomsday glacier." It also describes our first truly global climate catastrophe. This soon-collapsing massive glacier will give you a powerful glimpse into the global economic, social, and political turmoil that just this one major collapsing glacier will create as coastal real estate prices plummet.)

Not only do you have to be aware of the above rules, but today's real estate investors must also be aware of our rapidly deteriorating climate change conditions. Current projections are that climate change and global warming consequences will become significantly worse (25 to 40% worse) from 2025 to 2031 because of past crossed climate tipping points, new crossed climate tipping points, and climate feedbacks. (Please click here to read all about how and why this will happen, described in the first tipping point described on this page.)

The escalating global warming emergency has created new rules for the intelligent location or relocation of future personal or business real estate investment. Failure to include these minimal due diligence criteria in business real estate purchase evaluations will most likely expose those evaluators and companies to gross negligence lawsuits from angry shareholders or investors who experience the value of their investments or properties ravaged by currently known global warming consequences and established prediction patterns.

Additionally, many in real estate and related industries are also beginning to take note of escalating global warming’s total broader economic impacts of on their nation’s GDP (gross domestic product) and, conversely, on their own expansion plans, future risks, markets, and bottom lines. The current predictions for how high the total annual global warming-related costs to nations around the world will rise range from 5% of total gross domestic product (in the Stern report) to 10% of the total GDP (from the book Climate Shock) to up to 30% of the total GDP in escalating global warming’s final phases as described in the Climageddon Scenario in the new book Climageddon, The Global Warming Emergency and How to Survive It. It is not unreasonable to also project that similar GDP cost/loss annual operating percentages will eventually apply to the net incomes of those purchasing real estate in global warming high-risk zones --- if they can still get insurance.

In conclusion, few knowledgeable individuals or businesses will want to live, work, or buy homes or conduct business or be part of businesses in any of the rapidly enlarging global warming unsafe zones. Global warming is quickly evolving the time-tested real estate value adage of “location, location, location” to “always purchase your real estate or business investments in global warming-safe locations.”

If you are still investing in unsafe global warming zones, get out before you start taking huge losses as more and more people, and other businesses recognize how our escalating and now irreversible global warming will affect their real estate, businesses, future, and finances.

Welcome to our brave new real estate and business investment world, where chains of the 20 worst global warming-aggravated consequences endlessly increase in frequency, severity, scale, and cost and will endlessly eat into your bottom lines. This is because the one thing you can rely on with the escalating global warming emergency is that the 20 worst global warming consequences will regularly and always increase in frequency, severity, and scale!

(The stability of real estate prices in many countries is already being affected by the climate. This rising instability is in part due to the severe climate consequence prediction and remedial solution errors of the IPCC of the UN. Click here to read about how those serious prediction and remedy errors could affect future forecasts in this area.)

For answers to all of your remaining questions about climate change and global warming, click here for our new climate change FAQ. It has over one hundred of the most asked questions and answers about climate change.

If you want to understand the climate science and analysis procedures we used to present the above information, click here for a technical explanation of our climate research process.

Showing 3 reactions

Sign in with

There are far better places to buy much safer global warming resilience land. See part one of the job one for humanity plan on

Best,

Lawrence